Work in process (WIP) inventory is a key indicator of the health of your business’s supply chain. If your procurement process looks anything like the following three scenarios, you should track and calculate your WIP inventory.

- You’re in the business of custom, handmade goods, and you acquire raw materials to assemble your products yourself.

- You work with multiple suppliers to source materials and then send them to a manufacturer to assemble your finished goods.

- You partner with a single supplier/manufacturer that sources materials on your behalf and assembles your finished goods.

In all 3 of these scenarios, you have unfinished goods (or WIP inventory) at some stage of the manufacturing process.

Download Ware2Go’s eBook to find out how to win customers for life with fast fulfillment.

Continue reading to learn exactly what WIP inventory is, how to calculate it, why it matters, and how it fits into a healthy supply chain.

What Is Work in Process (WIP) Inventory?

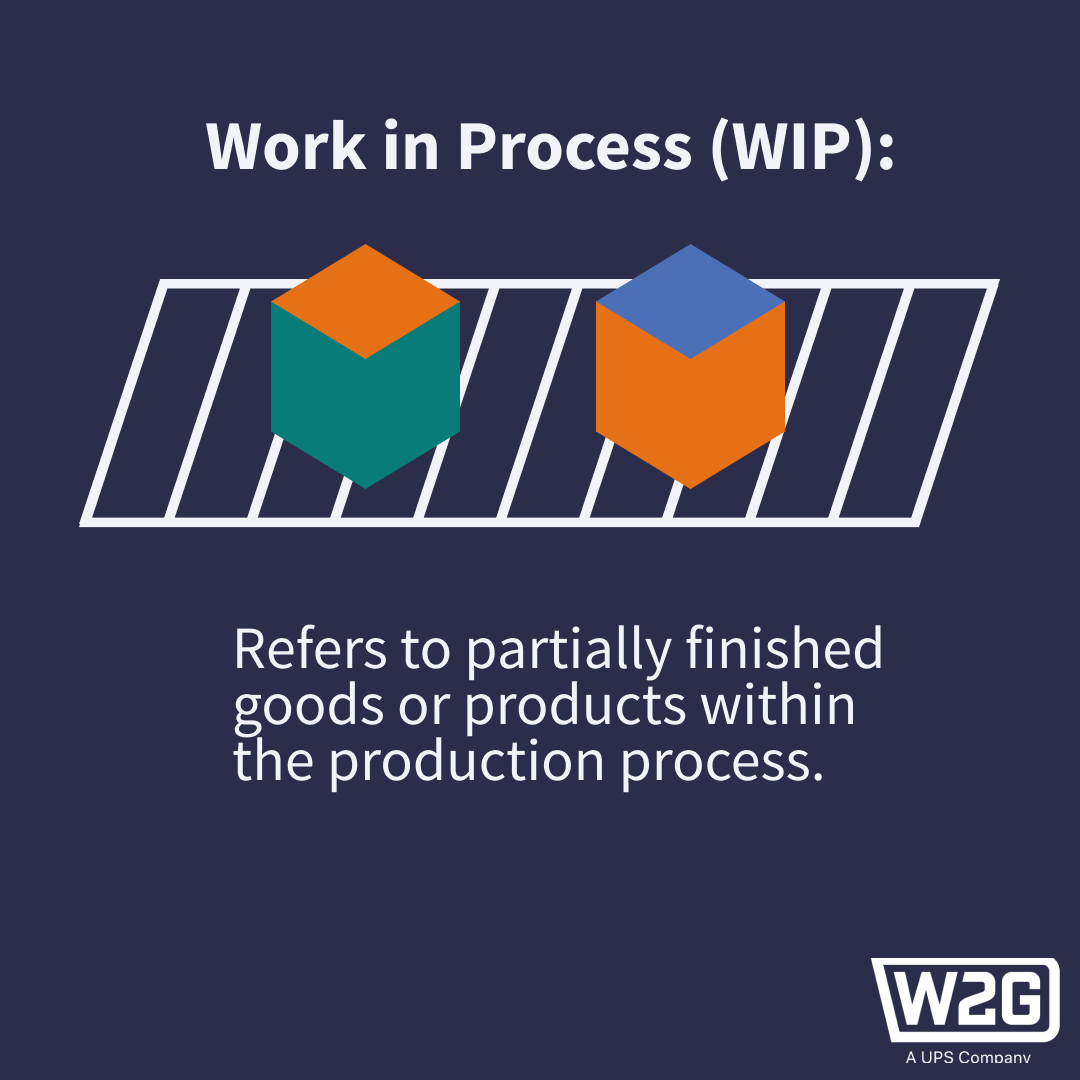

Work in process inventory refers to unfinished goods in the manufacturing process. WIP inventory represents the value of materials and labor invested in incomplete goods.

On any merchant’s balance sheet, the inventory line item comprises 3 types of inventory:

- Raw Materials: These are the materials used to assemble your product. For example, if you sell baking mixes, your raw materials are flour, salt, baking powder, etc., in the mix and packaging materials.

- WIP Inventory: These products are currently at some phase of the manufacturing process. They’re in an unfinished state, and, therefore, you cannot sell them. Once a raw material meets human labor, you should consider it a work in process.

- Finished Goods: These are your final assembled products ready for sale. Once an item sells, it’s referred to as ‘merchandise,’ and associated costs move to Cost of Goods Sold (COGS) in the accounting ledger.

So for accounting, WIP inventory is the total value of any unfinished goods, and although you can’t sell them, you should count these goods as a current asset on a balance sheet.

It’s important to include WIP inventory as a current asset when calculating your business value when finding investors, or securing financing. On the accounting side, calculating WIP inventory also helps you understand the true value of your inventory for tax purposes.

What’s more, calculating WIP inventory gives you a clear picture of the health of your supply chain so you can better optimize supply chain planning. Generally speaking, the best practice is to carry as little WIP inventory as possible. Too much WIP inventory on hand can indicate bottlenecks in your procurement or production process.

Work in Process Inventory Formula

Most merchants calculate their WIP inventory at the end of a reporting period (end of quarter, end of year, etc.) and when looking for their ‘ending WIP inventory.’ To calculate the ending WIP inventory, you need the beginning WIP inventory, which is the previous accounting period’s ending WIP inventory.

You must also calculate the production costs currently tied up in unfinished inventory. This includes the raw materials, labor, and overhead costs associated with the percentage of work completed.

Finally, you need the value of your finished goods, which is the total value of your inventory ready to sell. It includes manufacturing costs, raw materials, and overhead costs.

Once you have all of these variables determined, the formula for WIP inventory is as follows:

WIP Inventory Example:

Suppose your business calculates WIP inventory at the end of each quarter, and your accounting records show that your ending WIP inventory in the previous quarter was $15,000. In that case, that will be your beginning WIP inventory for the current quarter.

Then, you find that you’ve invested $225,000 in production costs for the quarter, and the total value of your finished goods is $215,000.

In this example, you would calculate your ending WIP inventory as follows:

($15,000 + $225,000) – $215,000 = $25,000

The Role of Work in Process (WIP) Inventory in the Supply Chain

Although you can’t see WIP inventory, it’s considered an asset on the balance sheet. For this reason, it’s best practice to hold as little WIP inventory as possible.

An excess of WIP inventory can be a symptom of congestion within the supply chain. Having excess WIP inventory on hand can also raise operating costs and reduce productivity in the following ways:

- You must store WIP inventory somewhere, and holding unsellable inventory for an extended period will increase inventory carry costs and drag down profitability. Free up storage space for finished goods that are ready to create revenue.

- WIP inventory represents capital tied up in raw materials and overhead costs. Holding as little WIP inventory as possible means you’re putting your capital back to work for you in the form of finished (sellable) goods.

- Unfinished products are at higher risk for loss or damage in the process.

WIP supports cost control and production planning by providing real-time visibility into production processes, allowing better resource allocation, identifying cost drivers, facilitating just-in-time production, optimizing scheduling, and ensuring quality control.

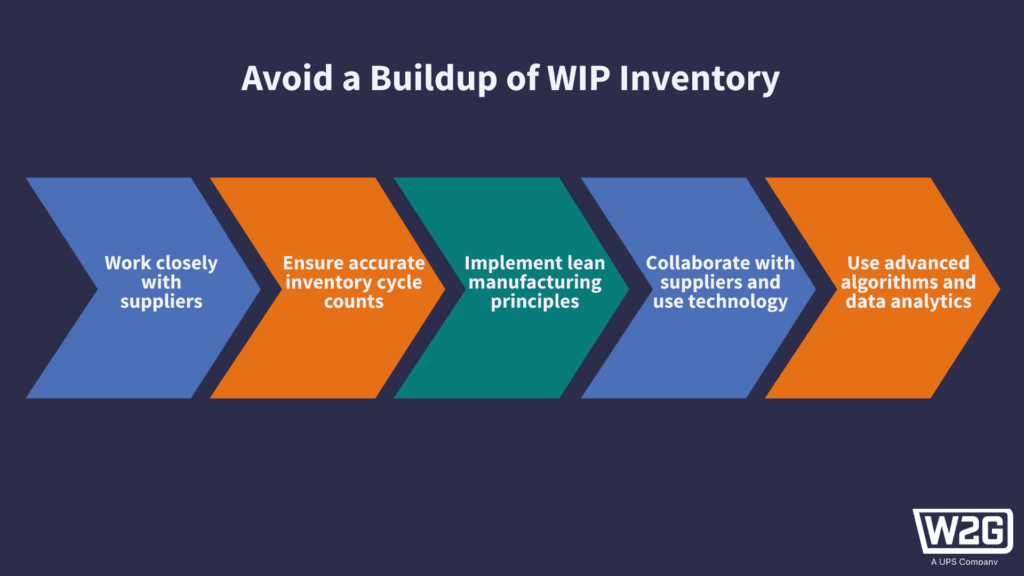

How to Avoid a Buildup of WIP Inventory

It’s particularly important to monitor supply chain efficiency during unprecedented supply chain disruptions leading to raw material shortages and extended lead times. These elevated lead times have led many merchants to forecast demand and procure inventory 6 months in advance (as opposed to historically forecasting every quarter).

- Work closely with suppliers for the most accurate projections of lead times possible.

- Ensure accurate inventory cycle counts. An integrated Warehouse Management System (WMS) can give you accurate, real-time inventory counts. This helps you build more accurate forecasts to communicate efficiently with suppliers and freight forwarders. Small to mid-size businesses can access enterprise-grade inventory management by outsourcing fulfillment to a 3PL or 4PL.

- Implement lean manufacturing principles, such as Just-in-Time (JIT) and Kanban, to improve inventory management. JIT ensures inventory is ordered and received only when needed for production, minimizing excess inventory and reducing inventory costs. Kanban, a visual scheduling system, signals when to reorder items based on consumption rates.

- Collaborate with suppliers and use demand-sensing technology to increase forecasting accuracy. By sharing data and insights with suppliers, businesses can develop more precise demand forecasts, reducing the risk of overstocking or stockouts.

- Demand sensing technology uses advanced algorithms and data analytics to analyze factors influencing demand, like sales data and market trends. This analysis allows businesses to adapt quickly to changing demands and optimize inventory levels accordingly.

What Is the Difference between Work in Progress and Work in Process?

While ‘work in progress’ and ‘work in process’ are often used interchangeably, they can sometimes refer to distinct situations. Typically, ‘work in progress’ refers to the costs linked with incomplete goods in the manufacturing process, encompassing raw materials, direct labor, and overhead expenses.

In accounting or financial reporting, ‘work in process’ refers to the value of partially completed goods or products within the production process.

In industries like construction, engineering, or software development, projects usually involve complex processes and multiple stages of completion. These time-intensive efforts are often referred to as “work in progress.” Planning, designing, testing, and reworking stages could take weeks, months, or even years to finish.

Work in process is a slightly different term for quickly manufactured goods.

Why Tracking WIP Inventory Is Essential

Work in process (WIP) inventory is crucial in industries where work is organized around specific projects rather than continuous production lines.

WIP inventory refers to the materials, components, and resources being transformed or incorporated into a project. This includes construction materials on-site, partially assembled equipment, or software code still being developed. In traditional manufacturing environments, inventory items move along a production line. In contrast, project-based WIP inventory is often spread across multiple locations and can involve diverse activities depending on the project.

This means that tracking WIP inventory becomes essential for managing costs, monitoring project processes, and ensuring the project is completed on time.

Here’s how WIP applies to many industries, its associated challenges, and methods used to track and integrate WIP inventory with project management software.

How to Track WIP Inventory

Use these methods to track work in process inventory accurately:

- Time and Materials Tracking: For projects billed on time and materials, tracking hours worked and materials used is essential to calculate project costs accurately. Time-tracking software and inventory management systems can help catch this data in real time, giving visibility into WIP inventory levels and project expenses.

- Job Costing: Costs are assigned to specific projects or tasks based on the resources used. This method tracks direct costs like materials and labor and indirect costs like overhead expenses. By linking costs with specific projects, organizations can accurately measure project profitability and allocate resources.

- Count Physical Inventory: Regularly counting and checking materials and equipment at project sites or warehouses gives project managers an accurate picture of inventory levels. Although it’s time-consuming, this step helps spot any discrepancies or potential issues with the inventory.

Integration with Project Management Software

Integrating WIP inventory tracking with project management software helps streamline project workflows and provides improved visibility into project progress and costs. Project management software often includes features for WIP tracking, allowing project managers to:

- Monitor Inventory Levels: Project management software can provide real-time data on WIP inventory levels, allowing project managers to make informed decisions about scheduling and resource allocation.

- Track Costs: Project managers can easily and quickly monitor costs and identify any overspending to reign in the budget and keep the project on track. The software can also identify any future potential cost overruns.

- Facilitate Collaboration: The software can centralize project-related information and allow team members to communicate with each other. The team can easily access schedules, assignments, and up-to-date inventory to improve the project’s efficiency.

Ware2Go’s Warehouse Management System, FulfillmentVu, offers over 250 plug-and-play eCommerce and retail integration technologies. These include warehouse management, transport flexibility, and advanced fulfillment capabilities that connect with Ware2Go’s 1–2 day delivery network. The warehouse management system market is set to grow from $4 billion in 2024 to $8.6 billion in 2029, highlighting its key role in supporting inventory management.

WIP Inventory FAQ’s

We’ve compiled some of the most commonly asked questions around work in process to provide more clarity:

What is Included in Work in Progress Inventory?

Work-in-process costs include all raw materials and labor needed to manufacture the finished product. Calculating WIP inventory is complicated because it requires assessing the cost of labor and overhead associated with the percentage of work completed.

Because it’s difficult and time-consuming to calculate, most merchants try to have as much inventory as possible in the finished goods stage before the end of a reporting period.

How Do You Calculate Work in Process Inventory?

There are three variables you need to calculate work in process inventory:

- Beginning Work in Process Inventory: You must have the previous quarter’s ending work in process inventory, which carries over as the next quarter’s beginning work in process inventory.

- Production Costs: This is a sum of your raw materials used, labor costs, and any overhead such as machine operating costs.

- Finished Goods: This is your total cost of goods manufactured (COGM), which is calculated by adding raw materials, direct labor, overhead, and beginning inventory work in process inventory, then subtracting ending work in process inventory.

Once you have all three of these variables, the formula for calculating WIP inventory is:

(Beginning WIP Inventory + Production Costs) – Finished Goods = Ending WIP Inventory

How Do I Account for Work in Progress Inventory?

Works in process (WIP) is included in the inventory line item as an asset on your balance sheet. The two other inventory categories are raw materials (the beginning materials used to manufacture a product) and finished goods (fully assembled products ready to be sold).

The Importance of Work in Process

Understanding and managing WIP inventory is key for businesses that want to maintain a streamlined supply chain and increase operational efficiency. By calculating WIP inventory, you can make informed decisions around production processes and reduce excess inventory.

With the correct strategies, you can leverage WIP inventory as an asset rather than a liability to meet consumer demands accurately.

Maintaining a healthy supply chain extends beyond inventory with smooth logistics to keep customers happy with fast fulfillment. As logistics experts, Ware2Go is well-positioned to help you better manage your supply chain with Ware2Go’s service.